We hebben Cato Corporation gekocht een familiebedrijf met dames mode winkels. 9% dividend, veel cash op het balans en geen schulden. Tevens een extra aandeel Tesla, dat pas goedkoop is als de groei een paar jaar evensnel zal gaan. De aankoop hiervan was terecht omstreden.

We hebben nu 20 aandelen, het streven is om 1 aandeel per machinist te hebben. De vraag is wat moeten/kunnen we nu verkopen?

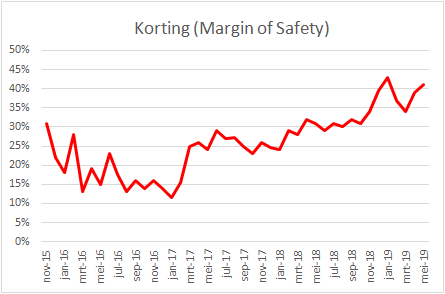

Doordat de koersen in januari gestegen zijn, is de Margin of Safety afgenomen. Het was veiliger om eind december 2018 aandelen te kopen dan vandaag.