It is 2 decades since the dotcom bubble and with hindsight it is easy to see how ridiculous market caps of Cisco Systems et al were in the year 2000 by using Peter Lynch charts.

Yesterday Jeff Koon's Rabbit was sold for $91m the highest price ever for a living artist, beating Hockney.

WeWork has filed for a >$50b IPO.

The company is seen as a competitor of Regus office space rental, but is also a social network based on the kibbutz and commune childhoods of the founders.

But just to get an idea of orders of magnitude, some back of the envelope math:

WeWork rents out 1m Square meters of office space. Say they earn a hefty net profit of €100/m per year, then earnings would be $100m multiple by a multiple of 20 and you get an intrinsic value guesstimate of $2b.

The IPO is 25x...

Another angle: WeWork has 400k members. What are investors paying per member?

Price $50b / 400k = One Hundred and Twenty-Five Thousand Dollars per member.

Life Time Value? Membership is $50 per month x 12 months is $600 per year. Times 10 = Six Thousand Dollars and that's Sales not Net Profit...

Also 25x too expensive.

One could argue WeWork is part of a "Unicorn" bubble. Check back in the year 2029. Also curious to see Aswath Damadorans take at Musing on Markets.

vrijdag 17 mei 2019

maandag 13 mei 2019

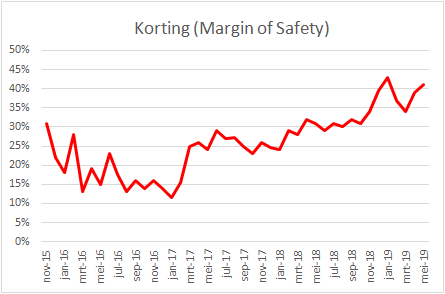

Stand mei 2019, Inleg €3 100, Graham Waarde €5 942, korting 41%

We hebben onder anderen NN Group bijgekocht en hebben weer Hibbett Sports gekocht.

dinsdag 26 maart 2019

Stand april 2019, Inleg €3 050, Graham Waarde €5 830, korting 39%

We hebben BMW3 Preferred shares bijgekocht onder €62, we hebben ASM International deels verkocht boven €48. De afschrijvingen op boekwaarde bij United Natural Foods (leverancier van supermarkten in de VS) viel mee na de overname van SuperValu. Hierdoor is de Graham waarde sterk gestegen in maart. We hebben een budget van €2 100 (inclusief te ontvangen dividenden) om aandelen (bij) te kopen. Thor Industries onder $60 is een mogelijkheid. Reliance Steel & Aluminium (ticker RS) heeft een 100% Graham Defensive score bij Validea en zit in de AAII screen.

donderdag 7 maart 2019

Corbion Benjamin Graham intrinsic value analysis

Expenses and long-term debt increased in 2018. The company is opening PLA plants in Thailand and Europe. I don't understand the business or prospects.

Benjamin Graham Defensive Analysis:

SECTOR: [FAIL] Corbion is a bio-technology company? and therefore Benjamin Graham would consider it too risky.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. Corbion's sales of €897 million, based on 2018 sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. Corbion's current ratio €350m/€260m of 1,3 is not good enough.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for Corbion is €185 million, while the net current assets are €90 million. Corbion fails this test.

SALES: [PASS] The investor must select companies of "adequate size". This includes companies with annual sales greater than €260 million. Corbion's sales of €897 million, based on 2018 sales, pass this test.

CURRENT RATIO: [FAIL] The current ratio must be greater than or equal to 2. Companies that meet this criterion are typically financially secure and defensive. Corbion's current ratio €350m/€260m of 1,3 is not good enough.

LONG-TERM DEBT IN RELATION TO NET CURRENT ASSETS: [FAIL] For industrial companies, long-term debt must not exceed net current assets (current assets minus current liabilities). Companies that do not meet this criterion lack the financial stability that this methodology likes to see. The long-term debt for Corbion is €185 million, while the net current assets are €90 million. Corbion fails this test.

LONG-TERM EPS GROWTH: [FAIL] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. Corbion's earnings have not increased much over the past ten years and it has made losses recently.

Earnings Yield: [FAIL] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. Corbion's E/P of 4% (using the average over the past 3 years Earnings) fails this test.

Graham Number value: [FAIL] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. Corbion has a Graham number of √(15 x €1,3 EPS x 1,5 x €8,9 Book Value) = €16

Dividend: €0,56/€27 = 2%

Conclusion March 2019: The stock doesn't seem cheap. Not for the Graham Defensive investor.

LONG-TERM EPS GROWTH: [FAIL] Companies must increase their EPS by at least 30% over a ten-year period and EPS must not have been negative for any year within the last 5 years. Companies with this type of growth tend to be financially secure and have proven themselves over time. Corbion's earnings have not increased much over the past ten years and it has made losses recently.

Earnings Yield: [FAIL] The Earnings/Price (inverse P/E) %, based on the lesser of the current Earnings Yield or the Yield using average earnings over the last 3 fiscal years, must be "acceptable", which this methodology states is greater than 6,5%. Stocks with higher earnings yields are more defensive by nature. Corbion's E/P of 4% (using the average over the past 3 years Earnings) fails this test.

Graham Number value: [FAIL] The Price/Book ratio must also be reasonable. That is the Graham number value must be greater than the market price. Corbion has a Graham number of √(15 x €1,3 EPS x 1,5 x €8,9 Book Value) = €16

Dividend: €0,56/€27 = 2%

Conclusion March 2019: The stock doesn't seem cheap. Not for the Graham Defensive investor.

dinsdag 5 maart 2019

Stand maart 2019, inleg €3 000, Graham Waarde €5 547, korting 34%

We hebben nu EUR 2 023 cash (126 per persoon). Budget is 100% in aandelen. Aankoop eind maart? Goede resultaten van onder andere ASM International, Miller Industries en Assured Guaranty drijft winst per aandeel en boekwaarde omhoog waardoor Graham Waarde stijgt.

vrijdag 22 februari 2019

Inner Scorecard 2018

Hou niet van schulden. Hoge schuld is hoge risico.

United Natural Foods =>opeens hoge schuld, dramatisch keldering

Outokumpo idem

BMW idem

Steinhoff idem

Een goed bedrijf produceert cash en neemt weinig risico's met hoge schulden.

Bayer veel schulden

Flexsteel ook een verliespost. Boekte winst door voorraad te produceren maar verkocht niets. Cash is king. Had ik niet meer van moeten kopen.

dinsdag 5 februari 2019

Stand februari 2019, inleg €2 950, Graham Waarde €5 462, korting 37%

We hebben Cato Corporation gekocht een familiebedrijf met dames mode winkels. 9% dividend, veel cash op het balans en geen schulden. Tevens een extra aandeel Tesla, dat pas goedkoop is als de groei een paar jaar evensnel zal gaan. De aankoop hiervan was terecht omstreden.

We hebben nu 20 aandelen, het streven is om 1 aandeel per machinist te hebben. De vraag is wat moeten/kunnen we nu verkopen?

Doordat de koersen in januari gestegen zijn, is de Margin of Safety afgenomen. Het was veiliger om eind december 2018 aandelen te kopen dan vandaag.

Abonneren op:

Posts (Atom)